Financial independence retire early is the ultimate goal for so many people.

This post contains affiliate links; please read our Disclosure for more information

This movement continues to gain traction over time and many would love to attain it.

The truth is, financial independence means different things to different people.

For us, it’s more than money.

Financial independence means time freedom.

The freedom to do what we want with our short time here on earth.

Let’s look into it further.

Table of Contents

Financial Independence

Financial independence is largely about having enough money to pay for your living expenses.

This money stops you from depending on a job to pay for your lifestyle by being independent.

Some call it financial freedom and it’s easy to see why.

In the book The Simple Path To Wealth, JL Collins talks about financial independence as F-You money.

This money gives you the power to say F-You to the things that no longer serve you, and simply walk away.

With the most likely person at the receiving end of this being your employer.

Why Aim For Financial Independence?

There are various reasons for financial independence.

You may hate having an employer telling you what you can and can’t do.

Or have ambitions to be more present in your family’s lives and not be held back by a career.

Others have dreams of doing philanthropy and volunteering work in other countries.

It’s the ultimate control of your life, time and energy.

There are various flavours of FI, with FIRE being the vanilla option that many aim for.

Financial Joy Academy is a platform where you can build your plan to achieve financial independence. Lindie and I are part of this thriving community and we’re on our path towards financial independence.

Check it out by clicking here (plus you’ll get a 15% discount if you join).

FIRE – Financial Independence Retire Early

We initially started aiming for FIRE after coming across it in Playing With F.I.R.E.

Although the book doesn’t give you a blueprint on how to achieve fire, it inspires you to play with FIRE.

Financial independence (FI) and financial independence retire early (FIRE) are often used interchangeably.

FI, as mentioned before, is about having financial independence from needing a job.

FIRE explicitly promotes the end goal of actually retiring early.

This means retiring years ahead of the typical retirement age of sixties or seventies.

There are people who aim for FIRE to retire as early as thirty years old.

FIRE Principles

The fundamentals of the FIRE movement are to earn more, spend less and invest the rest.

This requires you to set up a budget, eliminate all consumer debts and minimise your outgoings.

Then aim to save as much as you can towards your FI pot.

Most FI gurus preach low-cost index funds as the chosen home for this FI pot.

With FIRE, you’ll be investing a heavy sum, as substantial as 50-70% of your take-home pay.

This aggressive method is so you can have enough money to retire early.

How Much Do I Need To Retire Early?

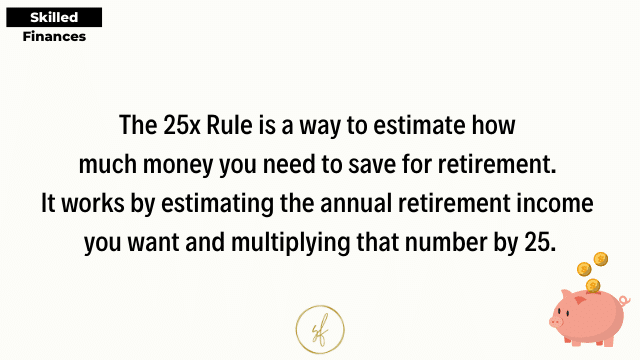

The popular barometer used is the 4% rule.

This states that you can withdraw 4% of your savings every year without running out of money for 30 years.

The value of your savings should be 25 times your estimated retirement annual expenses.

Let’s say you’ll need £30,000 per year (£2,500 per month) for your living expenses.

£30,000 x 25 = £750,000.

4% of £750,000 = £30,000.

This means your goal is to have £750,000 in your FI savings pot to retire early and have enough to live on.

But it’ll take the average person a long time to save that sum or attempt to, never mind more.

This is why the aggressive investing approach is the preferred method.

If invested in the stock market your FI pot will grow year on year through compounding interest, given that it’s invested for a long time period.

On average the stock market grows 8% per year, so withdrawing 4% means you’re taking out less than the growth amount.

Ok, let’s look into the other flavours of FIRE.

Fat FIRE

The second flavour of FIRE is Fat FIRE.

Some see this as FIRE on steroids.

This is where the goal is to retire with a more-than-average monthly income from the FI savings pot.

This may also be for high earners who are looking to keep a similar standard of lifestyle.

The plan is to build a beefy FI pot still following the 4% rule.

Some argue Fat FIRE is for those wanting at least £100,000 from their FI savings pot but I disagree.

FatFIRE is having an income that makes you live super comfortably, and you define what ‘fat’ means for you.

For instance, say you currently live on the £30,000 but you want double that in FIRE.

For you to have an annual income of £60,000 (£5,000 per month) the FI savings pot would be £1.5m.

On paper, this may not be classed as Fat FIRE but for you, you’d now have more money in retirement.

Fat FIRE is about having a much bigger pot to live comfortably and luxuriously in retirement.

Lean FIRE

You can probably guess what Lean FIRE is about right?

It’s the opposite of Fat FIRE.

This is where your aim is to live on just-enough during retirement.

You may be all things frugal, a minimalist or simply don’t feel the need for the ‘fat’ so you trim it down.

This also means your savings pot is also trimmed down from the standard FIRE pot.

For example, instead of £2,500 per month, you opt for £1,500 per month for your living expenses in retirement.

Your savings pot would need to have £450,000 in that scenario.

The point is, you’ve decided you want enough to pay for your bills in retirement.

You’d be happy to retire with just enough money that you’ll need to live well on a small income.

Barista FIRE

This approach is more of a relaxed approach to FIRE.

Barista FIRE is where you build up enough in your savings pot to cover some of your living expenses.

Your intention with Barista FIRE is to carry on working to cover the other portion of your living expenses not covered by your FIRE pot.

In simpler terms, it’s like a halfway house.

Your FI savings pot may have enough to cover essential bills whilst your job covers everything else.

This would suit you if you have no desire to start a business or leave employment early.

Barista FIRE puts you in a position to take on jobs you really want despite the pay.

Or leave the corporate world for the gig economy such as being a barista at a coffee shop – hence the name.

Or it empowers you to work part-time so you can spend more time with your family.

Keep in mind this is not complete financial independence as you’ll still need income for the other costs.

But it puts you in a position of power.

The power to choose how you earn that extra plus to do what you want knowing your bills are paid.

But more powerfully, it’s time freedom.

Even if it’s not full independence, it’s enough to make you live on purpose.

Coast FIRE

Similar to Barista FIRE, Coast FIRE takes on a relaxed vibe on the FI journey.

But there are some differences between the two approaches.

Coast FIRE is about investing enough early to be able to stop making contributions and still be financially independent in the future.

The day you stop making contributions is not the day you’ll be financially independent.

However based on calculations, compounding interest will carry on the rest of the journey for you.

Coast FIRE demands a pretty aggressive approach upfront to rapidly grow your investments.

However, once you reach that tipping point you can coast your way to FI.

Let’s go back to our example of needing £750,000 for an annual income of £30,000.

You’d need to leave £110,000 invested over 25 years to coast to FI.

A financial goal by 30 could be to coast to FI until the age of 55.

In action, between the ages of 20-30, the plan would be aggressively investing to build up £110,000.

Then from 30, they can leave it growing through compounding interest and passively get to FIRE.

This empowers you to only think about earning enough to live on as your future is covered for.

Again, this empowerment is the heart of all flavours of Financial Independence Retire Early.

FIOR – Financial Independence Optional Retirement

If early retirement is not one of your powerful reasons for financial independence, FIOR may be.

FIOR is ideal for those who love the idea of FI but early retirement is not a goal for them.

Maybe you don’t hate your job and actually enjoy what you do.

Work may be part of your identity and you may wish to progress your career further.

Maybe a reduction in working hours or a lower-level job is what would allow you to be there for your family.

Or you may wish to have more time to pursue other passion projects whilst keeping a part-time job.

Financial independence gives you the power to make the decisions that feel right for you.

You may think choosing Coast FIRE and Barista FIRE is a FIOR strategy.

But my take on this is you can choose any of the flavours above as this is more about your intentions.

Just because you reach FIRE on paper doesn’t mean you have to leave your job.

The ‘RE’ ingredient in all the flavours of FIRE is simply an outcome you could take by being financially independent.

Financial Joy Academy is a platform where you can build your plan to achieve financial independence. Lindie and I are part of this thriving community and we’re on our path towards financial independence.

Check it out by clicking here (plus you’ll get a 15% discount if you join).

Financial Independence Retire Early Summary

Regular FIRE is aiming to have an average lifestyle in retirement.

Fat FIRE aims to have more money in retirement over your essential expenses.

Lean FIRE is about covering the bare minimum of your living expenses through your FI pot.

Barista FIRE is where you are financially independent but need a small top-up for other expenses.

Coast FIRE is where you invest aggressively in the early days so you can leave your investments to compound on their own as they grow.

FIOR is for those who want to achieve FI but have no plans to retire early.

Take Action

Choose your flavour, which one are you aiming for?

Discuss your money goals with your (accountability and/or intimate) partner to make it real.

More importantly, put a plan in place for financial independence to retire early.

Share this to others if you found value in it and feel others should too.

Check out our Ultimate Money Plan to get in control of your money and smash your financial goals

Let us know how you’re getting along by getting in touch with us, we’d love to hear from you

Knowledge is powerless without action

So take action, and take care

Thando